My Name is Paul H Cosentino. I started this Blog in 2011 because of what I believe to be wrongdoings in town government. This Blog is to keep the citizens of Templeton informed. It is also for the citizens of Templeton to post their comments and concerns.

Paul working for you.

Saturday, December 30, 2017

California Supreme Court Set For Ruling That Could Cut Pensions For Public Workers

California Supreme Court Set For Ruling That Could Cut Pensions For Public Workers

For decades now public pensions have been guided by one universal rule which stipulates that current public employees can not be 'financially injured' by having their future benefits reduced. On the other hand, that 'universal rule' also necessarily stipulates that taxpayers can be absolutely steamrolled by whatever tax hikes are necessary to fulfill the bloated pension benefits that unions promise themselves.

Alas, that one 'universal rule' may finally be at risk as the California Supreme Court is currently considering a case which could determine

whether taxpayers have an unlimited obligation to simply fork over

whatever pension benefits are demanded of them or whether there is some

"reasonableness" test that must be applied. Here's more from VC Star:

At issue is the "California Rule," which dates to court rulings

beginning in 1947. It says workers enter a contract with their employer

on their first day of work, entitling them to retirement benefits that

can never be diminished unless replaced with similar benefits.

"Lots of people in the pension community are paying attention

to these cases and are really interested in what the California Supreme

Court is going to do here," said Amy Monahan, a University of Minnesota professor who studies pension law.

"For years, self-interested parties, overly generous promises

whose true costs were often shrouded by flawed actuarial analyses, and

failures of public leadership had caused unsustainable public pension

liabilities," his office wrote. A ruling is expected before Brown leaves office in January 2019.

Meanwhile, it's not just California taxpayers that have an interest

in the Supreme Court's decision as twelve other states also observe a

variation of the 'California Rule', said Greg Mennis, director of the

Public Sector Retirement Systems project at Pew Charitable Trusts. One

of them, Colorado, has walked it back a bit, he said, requiring "clear

and unmistakable intent to form a contract before pensions will be

contractually protected."

While a change to California's interpretation of its rule would not

automatically change legal precedents in other states, it could provide

the catalyst for lawmakers to test changes that they previously

considered unfeasible.

As we pointed out earlier this year, the case currently before the Supreme Court comes after a lower court ruled that "while

a public employee does have a ‘vested right’ to a pension, that right

is only to a ‘reasonable’ pension — not an immutable entitlement to the

most optimal formula of calculating the pension." Here's more from the Los Angeles Times:

The ruling stemmed from a pension reform law passed in 2012 by state

legislators. The law cut pensions and raised retirement ages for new

employees and banned “pension spiking” for existing workers.

Pension spiking has allowed some workers to get larger pensions by

inflating their pay during the period in which retirement is based —

usually at the end of their careers. In a ruling written by Justice James A. Richman, appointed by

former Gov. Arnold Schwarzenegger, the appeals court said the

Legislature can alter pension formulas for active employees and reduce

their anticipated retirement benefits.

“While a public employee does have a ‘vested right’ to a pension,

that right is only to a ‘reasonable’ pension — not an immutable

entitlement to the most optimal formula of calculating the pension,”

wrote Richman, joined by Justices J. Anthony Kline and Marla J. Miller,

both Gov. Jerry Brown appointees.

Of course, 'reasonable' can be a tricky term to define and for most union bosses it is synonymous with 'MOAR'....the only question is does the California Supreme Court agree?

****************************************

Accounting For Reality – Pension Funds Are in Big Trouble

Submitted by Taps Coogan on the 31st of May 2017 to The Sounding Line.

Here at The Sounding Line, we have written about the looming public sector pension fund crisis on a number of occasions (most recently here).

At the core of the problem is a growing difference between the amount

of money public sector workers are paying into pension funds and the

amount of money that they are receiving in benefits. In stark contrast

to private sector retirement plans, employee contributions to public

sector pension funds can be as little as 3% for the first 10 years of

work and nothing after, while benefits are often as much as 70% of their ending salary, for life.

It is self-evident that 3% of one’s salary for the first 10 years of

one’s career is not remotely enough money to support a pension equal to

70% of one’s ending salary every year for decades following retirement.

Without a tax payer backstop such a retirement plan would be

inconceivable. It should come as no surprise that the private sector

retirement plans, which are not tax payer backstopped, have much higher

employee contributions, lower benefits, and few if any unfunded

promises.

Traditionally, the difference between modest contributions and

generous benefits has been made up by three factors: increasing number

of workers contributing to the pension fund, large investment returns on

the pension fund assets, and tax payers. However, all three of these

factors appear unable to keep up with growing unfunded pension

liabilities.

As the baby boomer generation reaches retirement age, the number of

people collecting benefits from their pensions is set to surge while the

relative number of young people working is declining. Furthermore, ultra-low interest rates have dramatically lowered pension fund investment returns. According to a recent report from the Hoover Institution,

on average, public pensions (state, local and federal employee pension

plans) assume that they will achieve a risk free 7.6% return on

investment per year, every single year. In an era where actual ‘risk

free’ returns on sovereign debt such as 10 Year US treasuries is below

3%, this 7.6% expectation is ‘wildly optimistic,’ forcing pension funds

to chase returns in ever riskier asset classes.

According to the Hoover Institute, even with this ‘wildly optimistic’

accounting, US public pension funds are short $1.191 trillion dollars.

Worse yet, once the increasing risk profile of pension fund assets is

accounted for, and more realistic market values are applied to pension

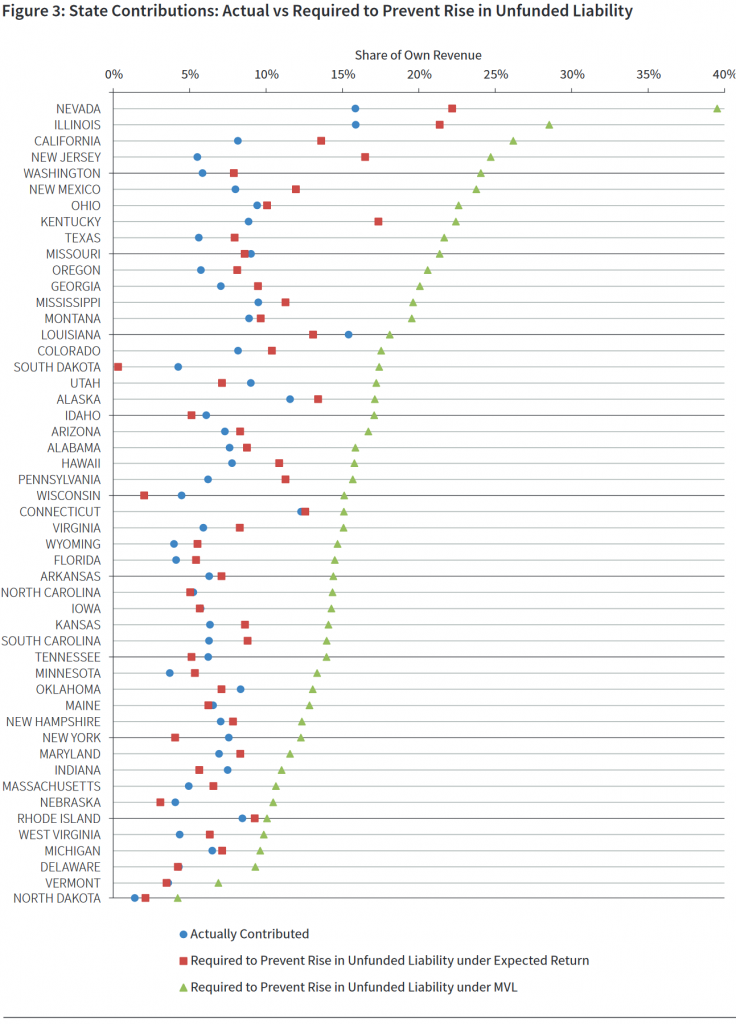

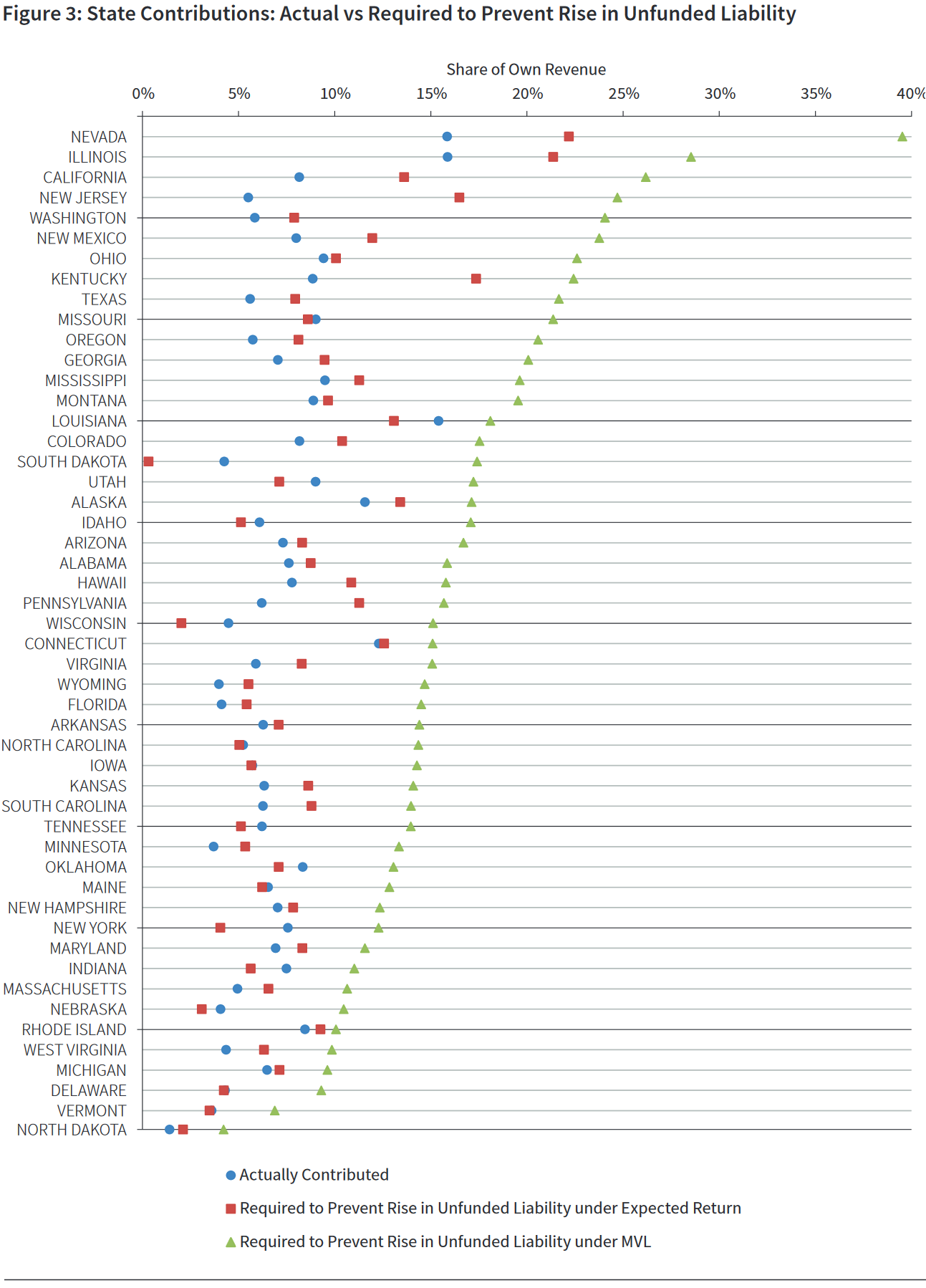

funds’ assets, the underfunding problem rockets higher. As the following

chart shows, using a more realistic market valuation of pension fund

asset values, the amount of additional contributions needed to keep

unfunded liabilities at pension funds across the US from rising even

further range as high as 39% of state tax revenues (the green indicator

is the percent of state tax revenues required)!

Chart Courtesy of the Hoover Institute

This brings us to the final problem for public sector pension funds.

Tax payers may no longer be able to make up the difference. Taxes in

many of the worst effected states are already at or near historic highs.

Raising tax rates far higher is not guaranteed to significantly raise

revenues, but is guaranteed to destroy jobs and slow growth (as Connecticut is already finding out).

Furthermore, it is questionable whether it is politically feasible to

continue raising taxes on private sector workers in order to fund far

more generous retirement benefits for far better paid public sector workers. Given these realities, and the reality that pensions represent the second largest element of average American household wealth, it is quite hard to conceive of a good ending to this problem for tax payers or for pensioners.

No comments:

Post a Comment